Efficient Practice Q&A Version

We understand our candidates have no time to waste, everyone wants an efficient learning. So we take this factor into consideration, develop the most efficient way for you to prepare for the REG exam, that is the real questions and answers practice mode, firstly, it simulates the real CPA Regulation test environment perfectly, which offers greatly help to our customers. Secondly, it includes printable PDF Format, also the instant access to download make sure you can study anywhere and anytime. All in all, high efficiency of REG exam material is the reason for your selection.

Outstanding CPA Regulation Study Materials

We know deeply that a reliable REG exam material is our company's foothold in this competitive market. High accuracy and high quality are the most important things we always looking for. Compared with the other products in the market, our REG latest questions grasp of the core knowledge and key point of the real exam, the targeted and efficient CPA Regulation study training dumps guarantee our candidates to pass the test easily. Passing exam won't be a problem anymore as long as you are familiar with our REG exam material (only about 20 to 30 hours practice). High accuracy and high quality are the reasons why you should choose us.

In this rapid rhythm society, the competitions among talents are growing with each passing day, some job might ask more than one's academic knowledge it might also require the professional AICPA certification and so on. It can't be denied that professional certification is an efficient way for employees to show their personal CPA Regulation abilities. In order to get more chances, more and more people tend to add shining points, for example a certification to their resumes. What you need to do first is to choose a right REG exam material, which will save your time and money in the preparation of the REG exam. Our REG latest questions is one of the most wonderful reviewing CPA Regulation study training materials in our industry, so choose us, and together we will make a brighter future.

One-year Free Update

In the era of information, everything around us is changing all the time, so do the REG exam. But you don't need to worry it. We take our candidates' future into consideration and pay attention to the development of our CPA Regulation study training materials constantly. Free renewal is provided for you for one year after purchase, so the REG latest questions won't be outdated. The latest REG latest questions will be sent to you email, so please check then, and just feel free to contact with us if you have any problem. Our reliable REG exam material will help pass the exam smoothly.

With our numerous advantages of our REG latest questions and service, what are you hesitating for? Our company always serves our clients with professional and precise attitudes, and we know that your satisfaction is the most important thing for us. We always aim to help you pass the REG exam smoothly and sincerely hope that all of our candidates can enjoy the tremendous benefit of our REG exam material, which might lead you to a better future!

AICPA CPA Regulation Sample Questions:

1. The uniform capitalization method must be used by:

I. Manufacturers of tangible personal property.

II. Retailers of personal property with $2 million dollars in average annual gross receipts for the 3

preceding years.

A) Neither I nor II.

B) II only.

C) Both I and II.

D) I only.

2. Clark bought Series EE U.S. Savings Bonds after 1989. Redemption proceeds will be used for payment of

college tuition for Clark's dependent child. One of the conditions that must be met for tax exemption of

accumulated interest on these bonds is that the:

A) Bonds must be bought by a parent (or both parents) and put in the name of the dependent child.

B) Bonds must be bought by the owner of the bonds before the owner reaches the age of 24.

C) Purchaser of the bonds must be the sole owner of the bonds (or joint owner with his or her spouse).

D) Bonds must be transferred to the college for redemption by the college rather than by the owner of the

bonds.

3. Smith made a gift of property to Thompson. Smith's basis in the property was $1,200. The fair market

value at the time of the gift was $1,400. Thompson sold the property for $2,500. What was the amount of

Thompson's gain on the disposition?

A) $0

B) $2,500

C) $1,300

D) $1,100

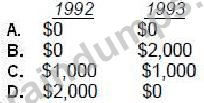

4. Smith, an individual calendar-year taxpayer, purchased 100 shares of Core Co. common stock for

$ 15,000 on December 15, 1992, and an additional 100 shares for $13,000 on December 30, 1992. On

January 3, 1993, Smith sold the shares purchased on December 15, 1992, for $13,000. What amount of

loss from the sale of Core's stock is deductible on Smith's 1992 and 1993 income tax returns?

A) Option B

B) Option C

C) Option A

D) Option D

5. Ryan, age 57, is single with no dependents. On July 1, 1997, Ryan's principal residence was sold for the

net amount of $500,000 after all selling expenses. Ryan bought the house in 1963 and occupied it until

sold. On the date of sale, the house had a basis of $180,000. Ryan does not intend to buy another

residence. What is the maximum exclusion of gain on sale of the residence that may be claimed in Ryan's

1 997 income tax return?

A) $320,000

B) $125,000

C) $0

D) $250,000

Solutions:

| Question # 1 Answer: D | Question # 2 Answer: C | Question # 3 Answer: C | Question # 4 Answer: C | Question # 5 Answer: D |

Kelly

Kelly

Edith

Edith

Hermosa

Hermosa  Harvey

Harvey

Edwina

Edwina  Sally

Sally  Myron

Myron  Leif

Leif  Otis

Otis  Cedric

Cedric  Phil

Phil  Buck

Buck  Sylvia

Sylvia  Ingrid

Ingrid  Gavin

Gavin  Belinda

Belinda  Emmanuel

Emmanuel  Hobart

Hobart  Adair

Adair  Montague

Montague  Ivy

Ivy